Sell-Everything Market Sends 60/40 Funds on Worst Run Since 2008

The classic 60/40 portfolio, a strategy named for the share allocated to equities and high-grade debt is on the worst ever run.

(Bloomberg) -- When practically everything is being sold off there’s almost nowhere to hide for investors, even those following one of the most conservative approaches out there.

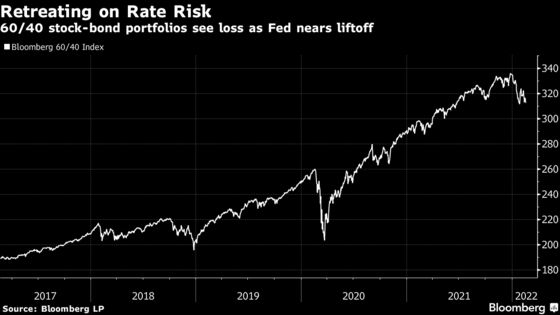

The classic 60/40 portfolio -- a strategy named for the share allocated to equities and high-grade debt, respectively -- is down more than 10% this year, leaving it on pace for the worst drubbing since the financial crisis of 2008. Unlike then, though, it’s not just growth that’s a worry. Assets are being hurt by the risk that a stagnant economic expansion will be coupled with persistent inflation, a combination that could cause poor returns -- or even losses -- to extend for some time to come.

The market dynamics that took place on Monday capture the dilemma in a nutshell: stock prices took a beating, but so did bonds, along with oil and other commodities. It was just one day, but it underscored how long-relied-upon correlations can break down in the current environment.

“You cannot count on the sort of investment returns seen over history for a period of time,” said Chris Brightman, chief investment officer at Research Affiliates. “Bond yields, dividend and earnings yields are at a low starting point and it means future returns will be low when compared to history.”

There was some relief for investors on Tuesday, as prices for both bonds and equities rebounded after sharp declines in the past week. A tone of consolidation came ahead of the Federal Reserve meeting concluding on Wednesday.

It’s not the first time analysts have questioned whether the 60/40 mix will hold up, with some casting doubt during the early months of the pandemic only to see it deliver large returns as stocks surged. Yet the combination of tighter monetary policy and rising consumer prices has led to mounting warnings to investors that such gains are unlikely to endure.

During the the so-called “lost decade” of the 2000s, the “60/40 portfolio generated a meager 2.3% annual return and investors would have lost value on an inflation-adjusted basis,” Goldman Sachs Asset Management’s Nick Cunningham, the vice president of strategic advisory solutions, wrote in October.

“The very good returns of the past decade mean that is important for investors to establish more realistic return expectations,” said Izabella Goldenberg, U.S. head of portfolio strategy at Goldman Sachs Asset Management. She said that may involve seeking returns in global equities and “in principle being diversified for the long term.”

The rallies of recent years were a boon to 60/40 portfolios, with rock-bottom interest rates pushing up both bond prices and stock valuations, particularly those of high growth companies. The mix delivered an average return of 18% from 2019 through 2021, according to data compiled by Bloomberg. Since 2000, the inflation-adjusted return has been around 7.5% on a rolling 12-month basis, according to Morningstar.

But the Fed’s plans to raise interest rates is now hitting bonds while higher oil and commodity prices are dragging down stocks by raising the specter of 1970s-style stagflation -- posing potentially sustained headwinds to both parts of the 60/40 strategy. The Nasdaq Composite Index has declined nearly 20% this year while a broad gauge of Treasuries has lost 4.7%, more than in any year since at least 1974. Investment-grade corporate bonds have also tumbled and are heading toward the worst quarter since 2008.

Andrew Patterson, senior economist at Vanguard Group Inc., said markets are verging on a period of low gains for the 60/40 portfolio. He estimated that annual returns over the next 10 years will be “south of 5% and our estimates have been grinding down in recent years, mainly driven by equities.”

The bond market is a key part of that. After an era of extremely loose monetary policy, starkly diminished bond yields mean interest payments are doing little to offset losses as prices decline. And even at current levels, real 10-year Treasury yields -- or those adjusted for expected inflation -- remain below zero.

Equity and bond prices falling together may be a feature of the inflation shock. In past eras of supply-driven inflation, government bonds failed to offset equity losses, as prices in both markets moved together, said Jean Boivin, head of the BlackRock Investment Institute.

“Investors will have to live with higher inflation and that will challenge the role of government bonds in a portfolio,” he said. “Central banks will find it harder to contain inflation and also harder to ease if economic growth slows materially.”

That inflation threat has made other assets potentially more alluring than bonds. Pacific Investment Management Co. recently recommended shifting a portion of 60/40 portfolios into in commodities to hedge against elevated inflation. “When inflation increases, asset values generally fall,” and “even a small allocation to commodities may materially improve the inflation protection of a traditional 60/40 stock/bond portfolio,” it said.

©2022 Bloomberg L.P.